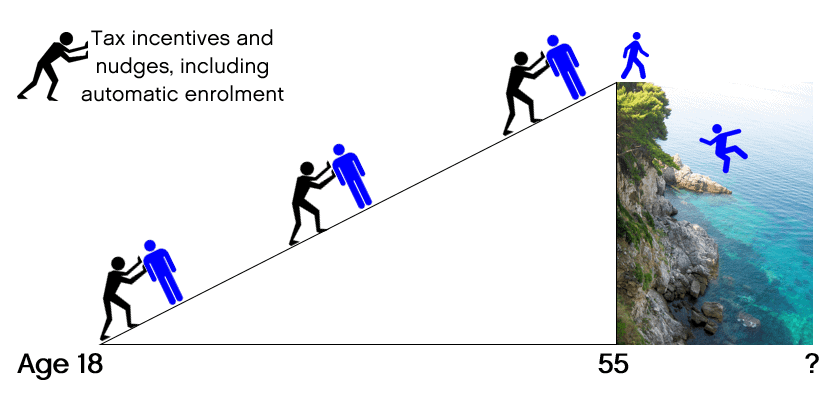

AUTO-PROTECTION

AUTO-DRAWDOWN AT 55, AUTO-ANNUITISATION AT 80

In 2010 the Centre for Policy Studies published “Simplification is the key“, which argued for the abolition of the requirement to annuitise, a proposal which came into law in April 2015.

However the CPS’ proviso that the abolition should take place “provided that both the state and the individual were protected from downside risks” appears to have been overlooked.

In a new paper, “Auto-Protection” published Thursday 23 March 2017 by the Centre for Policy Studies, Michael Johnson proposes the introduction of “auto-protection”, to complement auto-enrolment. The objective is the substantially reduce exposure to financial risks in later life, including premature exhaustion of savings, thereby also helping to protect the state. In addition, savers reaching the age of 55 would not be left to wallow in indecision when pondering the complexities of decumulation.

Auto-protection should have two distinct components:

- “auto-drawdown” at private pension age (currently 55, but the report recommends rapidly raising to 60), in the form of an income drawdown default of between 4% and 6% of pot assets, per annum. Providers should be encouraged to provide a low cost, diversified default fund for undrawn assets; with economies of scale helping to deliver larger retirement incomes than otherwise; and

- “auto-annuitisation” of residual pots, at age 80. This would facilitate the collective hedging of individuals’ exposure to the un-quantifiable risks of longevity. It would also remove later-life exposure to investment market risks and cost of living inflation.

The report’s author Michael Johnson notes that this should not be compulsory and does not in any way undermine the pension freedoms that have recently been introduced:

“To be clear, everyone should be free to opt out of one or both phases of auto-protection to pursue alternatives, consistent with 2015’s liberalisations. There is no desire to prevent people from doing what they want with their own savings.

The introduction of auto-protection would address a major policy inconsistency, whereby the state nudges and incentivises people to accumulate retirement savings, only to desert them at the start of decumulation.”

Michael Johnson concludes his report with a sobering warning:

“Any debate about what is the “right” form of defaults at 55 and 80 should not be

allowed to overshadow a more fundamental issue: the pots of most people at retirement are likely to be too small…We have to recognise that unless working life savings contributions are substantially increased (i.e. doubled), then many people are likely to run out of money before dying irrespective of the design of any retirement default.”

Click here to read the full report.

Media Coverage

- FT Adviser: Think tank pushes retirement income defaults