CORPORATION TAX TRIUMPH: LOWER RATES ARE LINKED TO HIGHER RECEIPTS

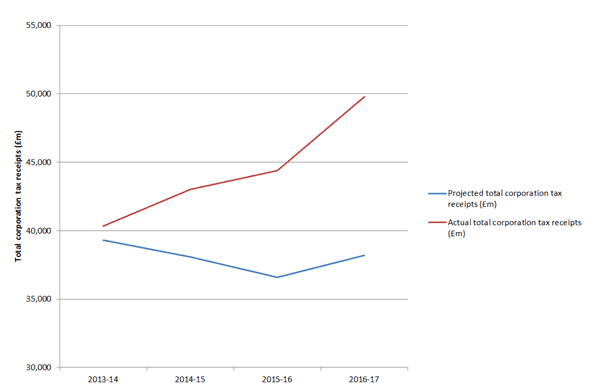

Statistics out this week show that onshore corporation tax receipts have increased by 44% since 2011-12, rising from £34bn to nearly £50bn in 2016-17. This has rapidly exceeded the Office for Budget Responsibility’s expectations in 2013, which projected that total corporation tax receipts would be just £38.2bn (see graph below).

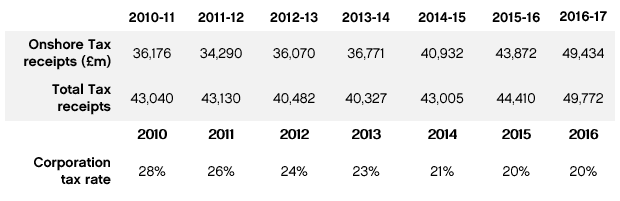

UK corporation tax receipts

Source: HMRC

Note 1: These figures exclude the Bank Levy and the Bank surcharge.

Note 2: Total tax receipts have seen a more modest rate of growth than onshore receipts due to the collapse in tax revenues from offshore North Sea oil and gas.

Projected total corporation tax receipts vs actual corporation tax receipts

Projected total corporation tax receipts come from the 2013 Office for Budget Responsibility Economic and Fiscal Outlook

This has occurred despite a cut in the headline rate of corporation tax from 28% to 20% over this period. Cuts in the headline rate of corporation tax since 2010 – as part of a raft of measures to increase competitiveness – have led to strong economic growth and higher profitability for companies. These in turn have helped to increase corporation tax receipts. This was originally advocated by the Centre for Policy Studies’ in David Martin’s paper “How to Cut Corporation Tax“.

The current government is planning to further reduce the corporation tax rate to 17% by 2020, which will give an additional boost the UK’s competitiveness. However, the paper “Why Corporation Tax Cuts Work“ by the CPS’ Head of Economic Research Daniel Mahoney – which has been updated following the publication of figures this week – highlights that Labour’s current commitments on corporation tax will undermine the UK’s competitiveness while leaving a series of unfunded spending commitments.

The Labour Party has publically stated that it would fund £15 billion worth of commitments by increasing the corporation tax rate to 21.5%. This will leave at least a £10 billion funding gap.

Responding to the corporation tax receipt figures, Daniel Mahoney said:

“The UK is now the 7th most competitive country in the world, up from 11th in 2010. This has been achieved by cuts to the corporation tax rate along with a raft of other measures.

This is a great achievement for the Government and the UK economy is reaping the rewards. The boost in competitiveness has led to buoyant corporation tax receipts – particularly onshore receipts – which have largely arisen from strong economic growth and higher profitability for companies.

This highlights the need to sustain the UK’s competitiveness by pursuing competitive rates of business taxation.

Labour’s plans on corporation tax and their associated pledges, on the other hand, would undermine the UK’s competitiveness and leave a series of unfunded spending commitments.”

Tim Knox, Director of the Centre for Policy Studies, added:

“Analysis set out in Why Corporation Tax Cuts Work demonstrates the failure to model accurately the dynamic effect of tax cuts. In 2013, shortly after the Budget, the OBR forecast that corporation tax receipts for 2016-17 would fall to £38.2 billion. In fact, in 2016/17, receipts were 30% higher than the original forecast, at £49.8 billion. HMT should recognise publicly that lower rates can lead to higher receipts and should urgently review the dynamic modelling it uses.”

This paper was originally published on 8 March 2017 under the title “The Case for Corporation Tax Cuts” and has been updated to include the most recent figures.