The Cost of Living Crisis

The cost of living squeeze is already hurting British households, and it’s only going to get worse.

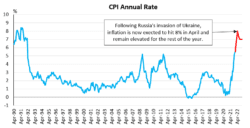

Inflation – which reached 5.5% in January – is outpacing wage growth, leading to a decline in real incomes. Interest rates are going up. At least two thirds of adults are reporting cost of living increases, with the overwhelming majority citing higher energy bills as the main cause.

This should come as no surprise. In our last Economic Bulletin, we noted that ‘Britain is entering into a cost of living crisis, with inflation on track to hit a 30-year high in the coming months even as taxes are going up’. However, thanks to Russia’s invasion of Ukraine, it is now clear that even that grim assessment was somewhat optimistic.

Previously, the consensus was that inflation would peak at around 7% in April, before gradually falling. Some forecasters now expect inflation to peak at around 8% in April, and remain at over 7% right the way through into 2023. The Resolution Foundation is projecting that real household incomes (for working households) will drop by over £1,000 y-o-y, the sharpest decline since the mid-1970s. The Centre for Economics Business Research, a consultancy, is predicting a fall in living standards of over £2,500 per household due to the fallout from the conflict.

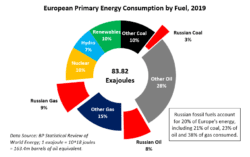

The geopolitical situation has sent global commodity prices skyrocketing. Although they have subsequently come down, both gas and oil have reached extraordinary highs in recent weeks. Russian gas is still flowing into Europe, but it’s anyone’s guess how long this is going to last. If the taps (pipeline and LNG) are turned off, 20bn cfd – equivalent to about 38% of Europe’s consumption – will disappear from the market. While the UK only imports a small amount of Russian gas (unlike Germany or Italy, for example) the knock-on effects will certainly be felt here.

Likewise with food. While we are not directly dependent on Ukrainian or Russian grains in the way some countries are, Ukraine and Russia account for around a quarter of global wheat exports. Farmers should be planting the next crop in Ukraine right now. But with tanks rather than tractors ploughing across the countryside, not much is getting sown. The impact on global food prices might be relatively limited for the time being, but it’s likely be a different story in six months’ time.

On top of this, economic sanctions imposed on Russia by Western and Asian democracies are going to cause supply chain disruptions across a widerange of sectors – semiconductors, aerospace, automotive, defence, chemicals – feeding into higher prices for consumers across the board. In addition to sanctions, many companies are voluntarily severing links with Russia, amplifying the disruption.

It’s also important to remember that global supply chain snarl-ups caused by Covid have not been resolved yet. Container ships are still queuing up 80-deep at major logistics hubs such as Long Beach and the Port of Los Angeles. Meanwhile, in its dogged pursuit of zero Covid, the Chinese state is flipping factories, ports and even whole cities on and off like switches on some giant macroeconomic switchboard.

In fact, China has just locked down Shenzhen, a conurbation of over 17m people and a major global technology and industrial hub, sometimes referred to as China’s Silicon Valley. The region hosts factories making components such as circuit boards, touchscreens and sensors ubiquitous in modern consumer durables.

The critical importance of Shenzhen to global supply chains is reflected in the fact that its container port is – in normal times – the fourth busiest in the world (by TEU volumes). Indeed, China hosts eight of the ten largest container ports globally, and 18 of the top 50. Disruption at Chinese ports is felt worldwide, feeding into delays, cost overruns and higher prices for consumers across a host of sectors in pretty much every economy.

Against this chaotic international backdrop, UK households are also facing the twin shocks of the energy price cap rising and a historic increase in taxation in April.

Given how drastically the macroeconomic outlook has changed since the Health and Social Care Levy was announced last October, it seems perverse to continue with a 1.25% NI rise that is going to make every working person in the country poorer. Moreover, with economic growth forecasts being hammered by the anticipated fallout from Ukraine, a tax on jobs and job creation looks even more ill-advised.

On the energy front, British consumers have so far been protected from the worst of record natural gas wholesale prices due to the energy price cap, with a swathe of energy companies going bust instead. From April, the average household annual energy bill will increase by £693 – a whopping 54% increase. But the energy price cap (which is rising from the equivalent of 63p/therm to 127p) will still be shielding people from market reality. The Government has announced measures to mitigate pressures on household finances in the short term, but April is not going to be end of the pain – far from it.

Even before the Ukraine crisis, natural gas prices looked likely to remain elevated for some time to come. Natural gas markets are grappling with a range of supply problems – not least underinvestment during the 2014-18 energy price downturn. At the same time, demand is surging: China’s long-term shift from gas to coal as part of its ‘Blue Sky’ anti-pollution initiative is a key driver here.

The one region where supply remains abundant is North America, where the fracking revolution has transformed the USA into an energy superpower. US natural gas is currently trading at less than a tenth of North Sea prices. Unsurprisingly, US shale gas has been touted as a solution to gas shortages in Britain and Europe.

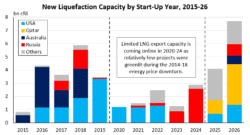

The problem, however, is getting it across the Atlantic. New liquefaction trains rampaging up at Sabine Pass and Calcasieu Pass will increase US liquefied natural gas (LNG) export capacity by 2.4bn cfd by the end of 2022. But that equates to just 5% of European gas consumption, and in any case, most of the volumes are already contracted to Asian buyers under long-term deals. After that, no new US liquefaction capacity is due onstream until 2025 at the earliest (again, this reflects cyclical underinvestment in the energy price downturn – LNG projects have very long lead times). In fact, of the 4.3bn cfd of LNG export capacity due onstream elsewhere over 2023-24, 80% is Russian.

Given the LNG bottleneck, and all other things being equal – including Russian gas still flowing into Europe at current volumes – European gas prices look likely to increase this coming winter and quite possibly again in 2023-24 and 2024-25. Household energy bills could easily go up by another £1,000 In October to around £3,000, according to the CEO of Energy UK, and things could be looking really quite dire indeed by October 2024.

Household budgets are going to come under pressure from lots of direction at once, but it is clear that energy is going to remain the biggest concern for most people, taking a big and very visible slice out of their discretionary incomes.

When it comes to volatile international energy markets, there’s not that much the Government can do in the immediate future, beyond properly targeted support for the people who are going to struggle the most. But thinking about how to tackle both high energy prices and cost of living pressures more broadly over the next few years should be among its very top priorities.

Targeted Short-Term Support

The Government has rejected the suggestion from us and others that it should cancel – or at least push back – the damaging increase to NI. We have therefore suggested an alternative plan to blunt the pain.

If the Treasury will not abandon the tax hike, it should at least compensate for its impact by increasing the threshold for paying employee NI. Raising the threshold to £11,284, instead of the planned £9,880, would completely protect low and median earners (those on £27,500 and below), limiting the impact of the tax to the most affluent deciles. The cost would be roughly £4.7bn of the planned £12bn.

This is far from a perfect solution – businesses and high earners would still pay more, damaging growth, and separate measures would be needed to address the impact of higher energy bills on the most vulnerable. But at least it would prevent the Government adding insult to injury.

The Government has already announced measures totalling £9.1bn to allow millions of households to reduce or defer some of the pain specifically from the energy price cap increasing in April. About 80% of households (those in council tax bands A-D) will receive a £150 council tax rebate from April. From October, around 28 million households will also automatically have £200 deferred from their electric bills. This will then be paid back in £40 instalments over five years (effectively functioning like an interest free loan).

However, much of this relief is poorly targeted. Council tax rebates – using bands still pegged to 1991 assessments – will not help all of the those who are least able to cope with the energy squeeze, while perversely, many relatively affluent people who can weather higher energy market prices will be protected. This is another of those policy areas where our Director’s argument that the most important part of modern government, and its most important limitation, is database management, comes into play.

If the Government decides to cushion the blow further this April, or when the energy price cap rises again in October, it needs to consider more targeted interventions. Crucially, these interventions should be ones that don’t risk adding permanently to Government spending – just look at how hard it was to reverse the temporary uplift to Universal Credit (UC) introduced during the pandemic.

A better model would be either a one-off payment to those already in receipt of any means-tested benefit, or the sort of clearly delineated ‘Coronavirus Hardship Payment’ recommended by the Centre for Policy Studies during the pandemic. Such approaches would avoid the distortions caused by using existing schemes, would be wide enough to help millions of people, but would not be throwing cash at those who can get through the next few years of high energy prices without it.

Moreover, to help ease the pressure on the poorest households, we should adjust benefit uprating periods to better mirror the accelerating rise in the cost of living. As things stand, inflation-linked benefits and tax credits will rise by 3.1% from April 2022, in line with the CPI rate of inflation in September 2021. The lag between uprating and price increases is going to leave millions worse off. We therefore suggest that the uprating should be brought forward, with lower increases once inflation has subsided in order to balance the books. As per Centre for Policy Studies recommendations, moving to a system of weekly benefit payments and cutting the waiting time for UC would also help to ease the pressures on those who are going to struggle the most.

To further reduce the pressure on the lowest earners, certain green levies should also be moved on to general taxation, saving another £155 on the average bill. Although part of the rationale of green levies on energy usage is to reduce overall energy consumption, this is a much less relevant consideration given current (and likely persistent) gas and electricity prices. This also makes the levies less distorting economically.

Ministers should also delay, or even write off, the charge of £70 per household being levied to cover the costs of energy companies that collapsed in Q4 2021 (although in the longer term, once energy prices are sustainably moving downwards again, the market-distorting energy price cap needs to be abolished).

In the short term, we should move the energy price cap calculations from a biannual to a quarterly basis, in order to avoid future shocks and allow households to plan better. According to a survey conducted by Ipsos-Mori on behalf of the Bank of England, the person on the street is expecting inflation of 4.3% this year. A lot of ordinary people are going to be in for a shock in April, when reality starts to bite.

Fixing the Energy Market and Growing the Economy

Regardless of whatever measures are taken to mitigate the impact of rising prices on households in the short term, the only long-term solution is to prioritise economic growth. That means making relatively clean energy as cheap as possible during the energy transition. It also means implementing a programme of radical supply side reforms to boost productivity growth across the economy.

The economic and fiscal modelling underpinning last October’s Budget depended on some pretty heroic assumptions about productivity growth, as we noted at the time in ‘The Age of the Trillion-Pound State’. But as it is only productivity growth that will deliver an increase in real wages, the task at hand is to achieve even firmer productivity growth against a far more challenging macroeconomic backdrop.

One way to reduce inputs relative to outputs in the production of goods and services (and to help household budgets) is to bring energy costs down. Yet as noted above, high gas prices are likely to persist for some years, given LNG capacity constraints and other international supply-demand dynamics. The problem is that other sources of energy are not going to help the UK much for the next few years either.

On the nuclear side of things, the 3.2 GW Hinkley C reactor is not scheduled to start up until 2026 (by which time 2.6 GW of capacity at Hartlepool and Heysham 1 will have shut down). There is talk of extending the life of 1.25 GW Sizewell B plant by 20 years, but this reactor is not in fact due to shut down until 2035. So, while a prudent and far-sighted measure, extending the operating life of Sizewell B is not really relevant to the situation at hand.

Meanwhile, the 1.3 GW Drax coal-fired power station has been mothballed and is slated for decommissioning this September; decommissioning has already begun at West Burton A (2 GW); and the other 2.1 GW of remaining coal-fired capacity in the UK is set to close by September 2024. It has been suggested that the lives of the Drax and West Burton A coal units could be extended. However, decommissioning is sufficiently far advanced – with coal stocks having been run down and staff having left or retired – that this is much easier said than done.

Moreover, renewables are only going to take up some of the slack. The Government has ambitious plans to expand the UK’s nameplate offshore wind capacity from 10 GW to 40 GW by 2030. But offshore wind farm projects are now facing severe delays and cost overruns due to ongoing economic disruption in China (China is the largest producer for many of the industry’s key components, dominating the supply chains for rare earth elements that go into wind turbine magnets). So even leaving aside intermittency issues, wind is going to be able to substitute only so much for gas-fired power generation over the next few years.

Clearly the UK needs to continue expanding nuclear and renewables provision in the coming years and decades, but neither energy source is going to be a panacea in the short term. That being said, there are still several courses of action open to us to ease the cost of living squeeze and minimise the need for to further bailouts or similarly expensive and unsustainable demand-side interventions.

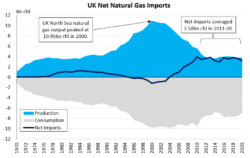

Firstly, we need to prioritise rebuilding gas storage capacity, so we can stock up as much as possible in the summer months in advance of the next few winters. Following the shutdown of Centrica’s Rough facility in 2017, the UK’s gas storage capacity is now just 53bn cf. That amounts to about five days of demand in a relatively mild winter (such as the one just gone). Other countries, such as the Netherlands and Germany, have enough storage capacity to meet at least 50 days of winter demand. As things stand, UK producers currently sell North Sea gas into the Netherlands in the summer months, partly for want of storage capacity here.

Increasing the gas storage buffer in line with the European average would help to shield consumers from price volatility and forestall the worst case scenario of rolling blackouts – a measure that should have been take years ago. And handily, repurposing natural gas infrastructure for hydrogen is quite easy, so new storage facilities and pipelines will not become stranded assets as the energy transition progresses. More natural gas storage capacity today will facilitate Net Zero tomorrow.

Secondly, we need to continue to support offshore exploration and production (E&P) activity in the North Sea. As part of this, the Government should look at accelerating regulatory approval for upcoming oil and gas projects such as Rosebank Ph.1, Clair South, Glengorm, Cambo and Bentley Ph.2, as it has indicated it will do. Approvals need to encompass both new developments and enhanced oil recovery (EOR) projects designed to eke out as much oil and gas as is economically feasible from mature fields.

Needless to say, a windfall tax on the sector is a terrible idea: taxing the companies that need to invest more in producing the gas we need would be completely self-defeating. Furthermore, many North Sea companies have already been left in a perilous position after years of low energy prices – running up debts and pushing cost deflation back up along the supply chain, impacting jobs and livelihoods. The North Sea oil and gas ecosystem is in an incredibly fragile state.

Looking a bit further ahead, as noted elsewhere, ‘if we want to develop and deploy planet-saving technologies such as wind, hydrogen and carbon capture in the North Sea, we need a robust industry and infrastructure’. Pulling the plug on the North Sea would be catastrophic for the UK’s energy transition. Fortunately, reports suggest the Government is also looking at plans for a new licensing round for offshore blocks – the first in the UK North Sea since 2019. This is welcome news.

However, the process from auction to offshore production takes years. Oil companies have to analyse seismic data, drill exploration wells and then, if they strike oil and or gas, drill and test appraisal wells. After that, they have to undertake pre-FEED and FEED studies on how they want to develop the field. Then, after obtaining regulatory approval for the field development plan and taking a final investment decision (FID), EPCI contracting, development well drilling and the actual construction of platforms and subsea structures can commence.

Depending on the size, geology and location of an offshore field, the time from FID to first oil/gas can take anything from half a year (for a very small, shallow water field tied-back to existing infrastructure) to over five years (for a complex, deepwater project in a harsh, remote area). Much of the UK’s remaining North Sea potential is in the West of Shetlands area, towards the more challenging end of this spectrum. So while more E&P activity in the North Sea should undoubtedly be encouraged, there aren’t actually that many quick wins here either.

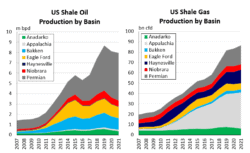

Thirdly, ministers could take a fresh look at boosting gas supplies through hydraulic fracturing of shale formations in the UK (while remaining prudently cautious about its economic and political viability).

Based on British Geological Society estimates, there is probably a few hundred trillion cubic feet of technically recoverable resources in the Bowland shale alone. Unfortunately, we have almost no idea of what percentage of these resources might be economically extractable reserves at any given gas price. This is because testing to date has been minimal. While the USA was busy being transformed into an energy superpower, the Coalition government caved in to the Russian-funded anti-fracking lobby and crushed the nascent UK shale sector beneath a mountain of regulations.

However, it seems that ministers are looking to keep the door open to fracking. The moratorium in place since 2019 is going to be reviewed, and Cuadrilla’s two exploration wells could be transferred to the British Geological Society for research purposes, instead of being plugged and abandoned. Authorising some limited drilling to better establish the potential of shale gas in the UK might not be the worst idea in the world, given the circumstances.

If it transpires that the reserves are there, some back-of-the-envelope calculations suggest that oil companies could ramp up UK shale production to 4bn cfd of shale gas within in 18-24 months, using 400 well pads taking up less than two square miles of surface area.

This is about six times slower than the rate at which the US shale sector can increase production under far weaker price incentives, but the UK would be starting virtually from scratch, and conditions are different here. Economies of scale are harder to achieve – densely populated Britain could fit into Texas alone almost three times over – while narrow roads and fewer options for pipelines represent non-trivial logistical constraints.

Nevertheless, even just this slow ramp-up to 4bn cfd would turn Britain into a net gas exporter (though given pipeline capacity constraints, much of that shale gas would have to stay in the UK market), adding about 8% to European gas supplies. Since high commodity prices are driven by moves at the margin, shale production in the UK could have a significant impact on reducing gas prices across the continent. This would gel with the leading role the UK has already played during the Ukraine crisis, helping various countries to take a firmer stance on Russia.

The domestic politics of fracking would remain fraught. Experts at the Royal Society and the Royal Academy of Engineering, among others, have thoroughly debunked arguments about fracking-induced earthquakes. But given the way public perceptions have been shaped by alarmist anti-fracking propaganda in recent years, bringing about a change in attitudes might be easier said than done.

However, if Lancashire residents living within 10 miles of a shale well were offered a suitable incentive – an 80% discount on their energy bills for five years, say, or even a direct cash payment – a lot of local opposition could melt away. This would be fiscally neutral, as the giveaways could be paid for the from the proceeds of shale block auctions and royalties on output. Any remaining revenue could go towards supporting households in the energy transition nationally, funding the accelerated installation of the heat pumps, hydrogen boilers and home insulation that will help reduce natural gas demand – the other side of the coin.

Fourthly, then, we need to think about the demand side: improving energy efficiency will, all other things being equal, result in other fuels being substituted for gas and in reduced energy demand in the longer run.

This means doing more to insulate our homes, and replacing gas boilers with heat pumps and hydrogen boilers. With gas prices as high as they are, homeowners have strong market-based incentives to investigate alternative heating sources when their existing boilers need replacing – incentives that are likely to persist for the next few years, given gas market fundamentals. However, there are things the Government can do around the edges to accelerate the process. An obvious one is reforming Energy Performance Certificates (EPCs) so they better reflect energy and carbon intensity, rather than the expense of heating a house.

When it comes to commercial properties, broader reforms to business taxation could also help to reduce gas demand. As recommended in a recent Centre for Policy Studies report, ‘Levelling Up and Zeroing In’, implementing ‘full expensing’ and a ‘green super deduction’ so businesses can invest in greener, more energy efficient tech would not only boost business investment in the UK, but help with energy security during the transition towards Net Zero.

Finally, looking beyond energy prices, we need supply side reforms to reduce some of the most significant costs that people face – such as housing and childcare – and unleash the productive potential of UK workers and businesses.

At the Centre for Policy Studies, we have put forward detailed policy proposals on how to free up housing markets, from reducing or eliminating stamp duty – a tax on mobility and aspiration – to measures designed to diversify housing and encourage new market entrants, products and customers.

Meanwhile, there are numerous ways the Government could create a business environment more conducive to investment and growth, from tax incentives to encourage British SMEs to expand into global markets, to measures such as ‘full expensing’ designed to reverse the UK’s declining international tax competitiveness and encourage greater investment in UK businesses and jobs. At the same time, it’s important to ensure that workers are able to pick up the skills and knowledge they need to pursue productive and satisfying careers.

Conclusion

Ultimately, whatever measures are politically necessary to alleviate the pain in the short-term, real growth in incomes comes from supply side measures that lower the cost of living. The alternative is to get trapped in a pattern of paying out taxpayers’ money to cushion people from cost of living pressures, without addressing any of the underlying causes. Quite apart from anything else, this is clearly unsustainable given the state of the public finances after Covid.

Above all, we need to avoid moving towards a disastrous prices and incomes policy. This would not do anything to help with inflation, but it would destroy the economic information contained in prices that markets need to function.

Things are looking bad – but the 1970s analogy only goes so far. For much of the 1970s, governments had to operate on razor-thin majorities, severely limiting their room for manoeuvre. The current Government has an 80-seat majority elected on a manifesto of low-tax, growth-oriented, post-Brexit dynamism. It should use this majority to enact the productivity-boosting reforms Britain so badly needs. Double-digit inflation, rolling blackouts and a new Winter of Discontent are far from inevitable. Even so, with the best will in the world, it’s going to be a tough few years before measures taken now start to have a big impact.

Karl Williams - Monday, 21st March, 2022

A data specialist with a background in energy and seaborne trade research in the City, his work at the CPS has focused on political economy, immigration policy and the intellectual foundations of free market conservatism - as well as content of the Thatcher Fellowship programme.