- On Friday, Kwasi Kwarteng is widely expected to cancel Rishi Sunak’s proposed rise in corporation tax from 19% to 25%

- New modelling by the US-based Tax Foundation and the Centre for Policy Studies shows that in the long term this will increase GDP by 1.2%, investment by 2% and wages by 1.1% compared to the higher-tax scenario

- However, this will be a case of avoiding a hit to GDP that would otherwise have taken place. The modelling shows that if Kwarteng goes further, and acts to incentivise business investment, he could increase long-run GDP by between 0.1% and 2.5%, depending on how ambitious he is

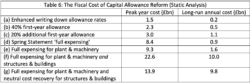

- The two think tanks have modelled the impact of various scenarios proposed by the Sunak Treasury, as well as the costs – and added further, more generous scenarios which extend capital reliefs to structures & buildings as well as plant & machinery

- Their modelling shows that the most generous of these options would increase long-term GDP by 2.5%, investment by 4.2% and wages by 2.1%, at an annual cost of approximately £10 billion a year

- They urge the new Chancellor to adopt the most generous regime possible, given the beneficial long-term impacts

Between 1995 and 2015, Britain had the lowest levels of business investment of all OECD nations. One explanation for this is that our tax system has been distinctly hostile to investment. The Tax Foundation’s 2021 International Tax Competitiveness Index ranked the UK 33 out of 37 OECD countries for ‘capital cost recovery’ – a measure of how well a corporate tax system treats investment.

The UK is also falling behind its European neighbours. In 2021, gross fixed capital formation in the UK was just 17.1% of GDP, compared to 22% in Germany and 24.4% in France.

New modelling by the US-based Tax Foundation and the Centre for Policy Studies in London shows that Kwasi Kwarteng’s widely reported decision to cancel the rise in corporation tax rise from 19% to 25% will be extremely beneficial to GDP, preventing a long-term hit to GDP of 1.2%, as well as a reduction of investment by 2% and wages by 1.1%.

However, the country is still set to be hit by a sharp deterioration in the attractiveness of the business investment regime, with the expiration of Rishi Sunak’s temporary ‘super-deduction’ in April.

The two think tanks have therefore modelled a wide range of alternatives to replace the super-deduction, including all of the proposals put forth by Rishi Sunak’s Treasury for consultation and review as well as two more ambitious options: full-fat ‘full expensing’, as previously recommended by the CPS, and full expensing which includes not just plant & machinery (as is the case with the super-deduction) but structures & buildings. This represents the most rigorous economic impact modelling of the options under consideration to date.

The research shows that the more ambitious and generous the Government is in terms of business investment, the greater the economic benefits. In particular, including structures & buildings within the capital allowances regime improves its benefits very significantly – but also drives up its costs.

The most radical option proposed by the paper would result in a 2.5% increase in long-term GDP compared to the regime that applied before the super-deduction, as well as a 4.2% increase in investment and 2.1% increase in wages, at a long-run cost of roughly £10 billion a year.

The two think tanks urge the Government to be as ambitious as possible, coupling a permanently higher Annual Investment Allowance with greater investment incentives above that. They also urge ministers to ensure that the new system is permanent, given the high levels of uncertainty for business that have resulted from allowances and incentives being raised and lowered so many times in recent years.

Tom Clougherty, CPS Head of Tax and co-author of the report, said:

‘The Government now has an opportunity to radically reform the UK corporate tax system.

‘There is no doubt that each of the reforms put forward would be an improvement. But by opting for the most radical option, full expensing, the Government will maximise business investment, boost productivity and deliver the higher levels of GDP growth that the country desperately needs. If growth is the goal, it pays to be as bold as possible.’

Daniel Bunn, Tax Foundation Executive Vice President, said:

‘Before the super-deduction, Britain ranked 30th out of 37 OECD countries when it came to the generosity of capital allowances – showing just how flawed its corporate tax system has become.

‘An aggressive, pro-growth tax agenda is the only way for the Government to deliver the long-lasting change the UK needs to emerge from its current slump. Being radical, introducing full expensing and extending it to structures and buildings is the only real answer for how to move forward.’

Tom is Head of Tax at the CPS. He was previously executive director of the Adam Smith Institute, before moving to the US to become managing editor at the Reason Foundation, and then a senior editor at the Cato Institute, the leading Washington think-tank.